2026 County Loan Limits for Conventional, FHA, VA, and USDA Home Financing

Nationwide Home Loans Group Provides Non-Conforming Solutions Up to $3 Million+

Written by the Nationwide Home Loans Group Lending Team | NMLS# 411500

Last Updated: November 30, 2025

Our lending professionals have originated mortgages across every loan program type for borrowers in all 50 states. Whether you need conventional financing, government-backed options through FHA or VA, rural property loans, construction funding, renovation capital, or refinancing, we guide clients through the full spectrum of mortgage programs available in today's market.

How the 2026 Conforming Loan Limits Affect Your Mortgage Options

The Federal Housing Finance Agency published updated conforming loan limit figures on November 25, 2025, establishing the maximum mortgage amounts that Fannie Mae and Freddie Mac can purchase for the coming year. These thresholds take effect January 1, 2026 and directly influence what financing options are available to you.

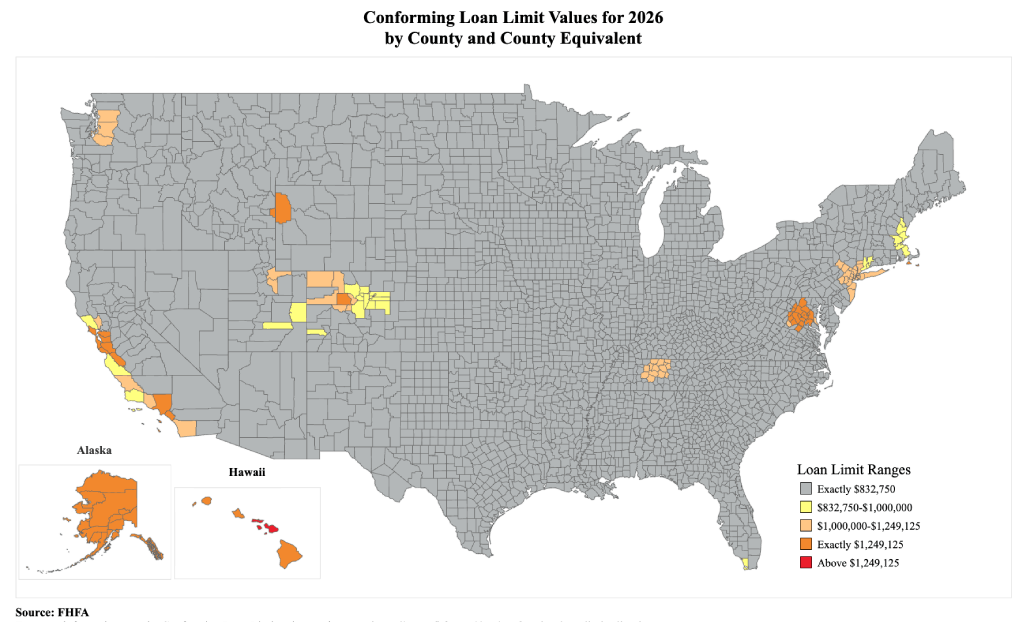

For 2026, the national baseline conforming limit increases to $832,750 for a single-family residence. This represents a $26,250 bump from the 2025 figure of $806,500, driven by a 3.26% rise in average home prices according to FHFA's House Price Index data. In counties where median home values push past certain thresholds, limits climb higher, reaching a maximum ceiling of $1,249,125 for one-unit properties.

Why do these numbers matter? Mortgages that stay within conforming limits typically qualify for better interest rates and smoother approval processes compared to jumbo loans, which exceed these caps and often require larger down payments, higher credit scores, and more documentation. Knowing your county's specific limit helps you understand what financing tier your purchase or refinance falls into and which loan programs make sense for your situation.

The sections below break down how these limits apply across conventional, FHA, VA, and USDA programs, along with what to do when your financing needs extend beyond standard thresholds.

2026 Conventional Conforming Loan Limits

Conventional mortgages backed by Fannie Mae and Freddie Mac follow the limits established by FHFA. These figures determine whether your loan qualifies as "conforming" (eligible for purchase by the government-sponsored enterprises) or "non-conforming" (requiring alternative financing structures).

Baseline Limits (Majority of U.S. Counties)

Over 3,000 counties across the United States use these standard baseline figures for 2026:

| Property Units | 2026 Baseline Limit |

|---|---|

| 1 Unit | $832,750 |

| 2 Units | $1,066,250 |

| 3 Units | $1,288,800 |

| 4 Units | $1,601,750 |

If you're purchasing a primary residence, second home, or investment property in most parts of the country, these baseline figures represent your conforming loan ceiling.

High-Cost Area Ceiling Limits

Roughly 155 counties qualify for elevated limits because their median home values exceed 115% of the national baseline. The FHFA caps these high-cost area limits at 150% of the baseline:

| Property Units | 2026 High-Cost Ceiling |

|---|---|

| 1 Unit | $1,249,125 |

| 2 Units | $1,599,375 |

| 3 Units | $1,933,200 |

| 4 Units | $2,402,625 |

Counties in metropolitan areas like San Francisco, New York City, Los Angeles, Seattle, and Washington D.C. typically sit at or near this ceiling. Many counties fall somewhere between baseline and ceiling based on their local median values. You can look up your specific county's limit through the FHFA Conforming Loan Limit lookup tool.

Alaska, Hawaii, Guam, and U.S. Virgin Islands

Federal statute grants these locations elevated baseline limits, recognizing the higher costs of construction and living. The baseline in these areas starts at 150% of the national baseline, with a ceiling reaching 150% of that elevated figure:

| Property Units | 2026 Baseline | 2026 Ceiling |

|---|---|---|

| 1 Unit | $1,249,125 | $1,873,675 |

| 2 Units | $1,599,375 | $2,399,050 |

| 3 Units | $1,933,200 | $2,899,800 |

| 4 Units | $2,402,625 | $3,603,925 |

2026 FHA Loan Limits

FHA mortgages follow a related but distinct limit structure. The Department of Housing and Urban Development calculates FHA limits as percentages of the FHFA conforming figures: the floor sits at 65% of the conforming baseline, while the ceiling matches the conforming high-cost maximum.

FHA Floor Limits (Low-Cost Markets)

In areas where median home values fall below national averages, FHA limits default to the floor:

| Property Units | 2026 FHA Floor |

|---|---|

| 1 Unit | $541,288 |

| 2 Units | $693,063 |

| 3 Units | $837,720 |

| 4 Units | $1,041,138 |

FHA Ceiling Limits (High-Cost Markets)

In expensive markets, FHA limits can reach the same ceiling as conventional high-cost limits:

| Property Units | 2026 FHA Ceiling |

|---|---|

| 1 Unit | $1,249,125 |

| 2 Units | $1,599,375 |

| 3 Units | $1,933,200 |

| 4 Units | $2,402,625 |

Most counties land somewhere between floor and ceiling, with specific FHA limits calculated based on local median values. FHA financing appeals to first-time buyers and borrowers who benefit from lower down payment requirements and more accommodating credit standards than conventional programs demand.

FHA Limits for Special Statutory Areas

Alaska, Hawaii, Guam, and the U.S. Virgin Islands receive even higher FHA limits:

| Property Units | 2026 FHA Special Area Limit |

|---|---|

| 1 Unit | $1,873,688 |

| 2 Units | $2,399,063 |

| 3 Units | $2,899,800 |

| 4 Units | $3,603,938 |

How VA and USDA Loans Differ from These Published Limits

The conforming loan limits published by FHFA govern conventional and FHA financing directly. However, two other major government-backed programs operate under different frameworks that borrowers frequently misunderstand.

VA Loan Entitlement Explained

Since the Blue Water Navy Vietnam Veterans Act became effective January 1, 2020, VA home loans no longer impose a strict maximum for veterans who possess full entitlement. If you've never used your VA benefit, or you've restored it completely after selling a property and paying off the associated VA loan, you can finance above any county limit with zero down payment, subject to meeting lender qualification standards.

The county conforming limits remain relevant for veterans with partial entitlement, specifically those who have an existing VA loan, experienced a foreclosure that affected their entitlement, or otherwise have some portion of their benefit tied up. In these situations, the FHFA county limit factors into calculating available guaranty coverage, potentially requiring a down payment on amounts exceeding remaining entitlement.

For comprehensive guidance on VA loan programs, including construction, renovation, and high-value purchases, our specialists at VA Nationwide focus exclusively on serving veterans and military families.

USDA Loan Qualification Framework

USDA Rural Development loans work differently altogether. Rather than applying county-based loan caps like conventional or FHA financing, USDA eligibility centers on household income (typically limited to 115% of area median income), debt-to-income ratios, and whether the property sits within a USDA-designated rural area.

While USDA does reference area loan limits for certain internal calculations, the primary constraints are income caps and geographic requirements rather than purchase price ceilings tied to conforming limits. If you're exploring rural property purchases, our dedicated team at USDA Nationwide can determine whether this program fits your situation.

Financing Options for Manufactured, Modular, and System-Built Homes

Factory-built housing, including manufactured homes, modular construction, and alternative building methods like SIP panels, metal frame structures, barndominiums, and ICF construction, follows the same conforming loan limits as traditional site-built properties when financed through conventional programs.

The key distinctions lie not in the limits themselves but in specific eligibility requirements: HUD certification for manufactured homes built after June 15, 1976, permanent foundation requirements, age restrictions (often 15-20 years maximum), and proper land ownership or lease arrangements.

FHA Title II loans for manufactured homes classified as real property use the same FHA floor and ceiling limits described above. FHA Title I loans, which cover chattel financing and certain combination loans, operate under separate HUD-established limits.

For buyers navigating the specific requirements of factory-built home financing, Manufactured Nationwide provides specialized expertise in these programs.

Historical Conforming Loan Limit Trends (2021-2026)

Tracking how limits have evolved provides perspective on housing market trajectory and helps borrowers understand shifts in purchasing power over time.

| Year | 1-Unit Baseline | 1-Unit High-Cost Ceiling | Year-Over-Year Change |

|---|---|---|---|

| 2021 | $548,250 | $822,375 | +7.42% |

| 2022 | $647,200 | $970,800 | +18.05% |

| 2023 | $726,200 | $1,089,300 | +12.21% |

| 2024 | $766,550 | $1,149,825 | +5.56% |

| 2025 | $806,500 | $1,209,750 | +5.21% |

| 2026 | $832,750 | $1,249,125 | +3.26% |

The 3.26% increase for 2026 marks the slowest annual growth since limits began climbing again after the 2008 housing correction. This moderation reflects stabilizing home price appreciation according to FHFA's third-quarter House Price Index data.

Multi-Unit Baseline Progression (2024-2026)

| Year | 1 Unit | 2 Units | 3 Units | 4 Units |

|---|---|---|---|---|

| 2024 | $766,550 | $981,500 | $1,186,350 | $1,474,400 |

| 2025 | $806,500 | $1,033,000 | $1,248,150 | $1,551,250 |

| 2026 | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

Investors considering multi-unit properties can use rental income from non-owner-occupied units to help qualify, making duplexes, triplexes, and fourplexes attractive wealth-building vehicles within conforming loan parameters.

What Happens When Your Loan Exceeds the Limit

When your financing needs surpass your county's conforming threshold, you enter jumbo loan territory. Jumbo mortgages, also called non-conforming loans, typically involve stricter qualification criteria: higher credit score minimums, larger down payment requirements, more extensive income documentation, and potentially higher interest rates depending on market conditions.

Nationwide Home Loans Group, through our Preferred Partners network, offers non-conforming solutions up to $3 million and beyond. We also provide one-time and two-time close construction loans that can accommodate both conforming and jumbo financing scenarios, combining construction and permanent financing into a single loan with one closing.

If your purchase price or refinance amount exceeds standard limits, our team can evaluate whether jumbo financing, portfolio lending, or alternative structures make the most sense for your circumstances.

Frequently Asked Questions About 2026 Loan Limits

What is the 2026 conforming loan limit?

The 2026 baseline conforming loan limit is $832,750 for a one-unit property in most U.S. counties. This represents a 3.26% increase ($26,250) from the 2025 limit of $806,500. High-cost areas can reach $1,249,125, and special statutory regions (Alaska, Hawaii, Guam, U.S. Virgin Islands) have baseline limits starting at $1,249,125 with ceilings up to $1,873,675.

How are county loan limits calculated?

FHFA determines county limits using local median home values within metropolitan or micropolitan statistical areas (CBSAs). When 115% of the highest median home value in a county's statistical area exceeds the national baseline, that county qualifies for an elevated limit capped at 150% of the baseline. The FHFA publishes complete county-by-county data each November.

What is the difference between conforming and FHA limits?

Conforming limits apply to conventional loans purchased by Fannie Mae and Freddie Mac. FHA limits, set by HUD, are calculated as percentages of conforming limits: the floor equals 65% of the conforming baseline ($541,288 for 2026), while the ceiling matches the conforming high-cost maximum ($1,249,125). Your county's specific FHA limit falls somewhere between these figures based on local median values.

Do VA loans follow these limits?

For veterans with full entitlement, VA loans have no maximum limit since January 2020. Qualified veterans can purchase above any county limit with zero down payment. Veterans with partial entitlement still reference county limits when calculating available guaranty coverage, which may affect down payment requirements on higher-priced properties.

How do USDA loan limits work?

USDA Rural Development loans don't use county-based loan caps like conventional or FHA programs. Eligibility depends on household income (generally 115% of area median income or below), debt-to-income ratios, and property location in USDA-designated rural areas. The conforming limits on this page don't directly constrain USDA financing.

When do the 2026 limits become effective?

The 2026 conforming loan limits take effect January 1, 2026. Loans delivered to Fannie Mae or Freddie Mac on or after that date follow the new limits. Loans closing in late December 2025 typically fall under 2025 limits unless delivery occurs in the new year.

Can conforming loan limits ever decrease?

No. Under the Housing and Economic Recovery Act of 2008, conforming loan limits cannot decrease. If home prices decline, limits remain flat until appreciation exceeds previous peaks. This protection applies at both national and county levels, providing stability for borrowers and housing markets.

What are jumbo loans?

Jumbo loans, also called non-conforming loans, are mortgages that exceed the conforming limit for a given county. Because Fannie Mae and Freddie Mac cannot purchase these loans, they typically require stronger credit profiles, larger down payments, and more documentation. Interest rates on jumbo loans vary based on market conditions and lender policies.

Do these limits apply to construction loans?

Yes. When the permanent financing for a construction project will be a conforming mortgage, the total loan amount must fall within your county's limit. One-time and two-time close construction loans that combine building and permanent financing in a single transaction follow the same conforming thresholds. Projects exceeding these limits require jumbo construction financing.

How do I find my county's specific limit?

The FHFA publishes a searchable database of county-by-county limits each November. You can access the official 2026 figures through the FHFA Conforming Loan Limit page. Our lending team can also identify your county's limit during initial conversations about your financing needs.

Do loan limits affect refinancing?

Yes. When refinancing, your new loan amount must fall within current conforming limits to qualify as a conforming loan. If your existing balance plus any cash-out exceeds your county's 2026 limit, you would need jumbo refinancing. Conversely, the higher 2026 limits may allow some borrowers with previous jumbo loans to refinance into conforming products, potentially accessing better rates.

Why did limits increase less in 2026 than in previous years?

The 3.26% increase for 2026 reflects moderating home price growth measured by FHFA's House Price Index. After increases of 18.05% (2022), 12.21% (2023), 5.56% (2024), and 5.21% (2025), the slower pace indicates a stabilizing housing market rather than the rapid appreciation seen in recent years.

Connect With Our Lending Team

Understanding loan limits is the starting point for mapping out your mortgage strategy. The right financing structure depends on far more than just these thresholds: your income, credit profile, down payment resources, property type, and long-term goals all factor into which program delivers the best outcome.

Nationwide Home Loans Group brings together expertise across conventional, FHA, VA, and USDA programs, plus construction financing, renovation loans, refinancing options, and non-conforming solutions for borrowers whose needs extend beyond standard limits. Our lending team has guided borrowers through every market condition and property scenario imaginable.

Ready to explore your options? Call us at 844-999-0639, start a chat conversation, or use our on-page eligibility quiz below to get the process moving. We'll help you understand exactly how your county's limits affect your plans and which financing path makes the most sense for you.

Sources and Official References

The loan limit figures on this page are sourced from official government publications:

Federal Housing Finance Agency (FHFA), "Conforming Loan Limit Values for 2026," published November 25, 2025. Available at fhfa.gov/CLL

FHFA 2026 Conforming Loan Limit Addendum (calculation methodology)

FHFA Conforming Loan Limit FAQs

FHA loan limits are calculated based on HUD guidelines using 65% of the conforming baseline for floors and 150% for ceilings. Official FHA limits are published by the Department of Housing and Urban Development.

Disclaimer: The figures on this page reflect FHFA's November 2025 announcement for 2026 conforming loan limits. Specific county limits and program details may vary. Always verify current guidelines with a loan officer, as program rules and lender requirements can change.

About Nationwide Home Loans Group

Nationwide Home Loans Group, powered by The Federal Savings Bank (NMLS# 411500), provides mortgage financing across all major loan programs for borrowers in all 50 states. Our team originates conventional, FHA, VA, and USDA loans, along with construction financing, renovation programs, refinancing, HELOCs, and non-conforming solutions for specialized borrower needs.

We maintain an A+ rating with the Better Business Bureau and have earned recognition from industry publications for our expertise in construction lending and specialized mortgage programs. Our loan officers hold individual NMLS licenses and complete ongoing education to stay current with program guidelines and regulatory requirements.